Many South African investment institutions, funds, banks and high net worth individuals, including their respective advisors, do not have at their immediate disposal the skill sets required for evaluating the fundamental risk-reward decision-making principles and process for investment in the upstream oil and gas industry. This is perfectly understandable due to its complexity, but often results in world-class exploration investment opportunities in South Africa being missed resulting in capital having to be raised in more developed foreign markets.

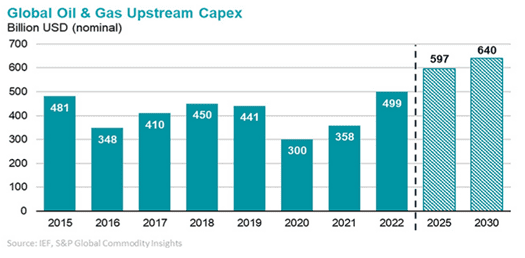

Many of the top companies in the world – by market capitalisation – have their roots in multi-jurisdictional oil and gas exploration. The International Energy Forum (IEF) in its latest report anticipates a significant increase in oil and gas upstream capital expenditures over the next 7 years. Furthermore, the IEF states that a cumulative US$4.9 trillion will be needed between 2023 and 2030 to meet market needs and prevent a supply shortfall, even if demand growth slows toward a plateau.

A critical success factor of the upstream oil and gas industry is to manage the exploration risks, both above and below the surface. A number of misconceptions exist which preclude many potential investors from even considering investment opportunities in the upstream oil and gas industry as viable given the potential of significant returns.

Set out below is an attempt to address and dispel some of these misconceptions. These are by no means exhaustive:

1. Investment in exploration is long term and money is only made after development when production is sold.

Successful exploration companies are focused on taking low value assets with adequate exploration potential, de-risking them with prudent expenditure programs to gather and analyse adequate scientific evidence that informs the balance of probable success during production and, thus, moving these assets up the value chain.

The most significant growth in capital value takes place during the exploration phase, if successful in each phase. Capital for further exploration is often raised through dilution or the sale of ownership interests in these assets. It is not uncommon for many oil and gas exploration companies to invest in initial exploration; to then dilute their position to recover past costs at a premium; and then to retain a carried interest going forward.

As proof of increased value, exploration companies will typically engage competent third parties to validate or invalidate the initial assumptions in their independent resource and reserve reports to demonstrate this increase in value within margins of error that have been considered as scientifically acceptable, based on norms and standards that have been developed over more than a century by industry experts.

Once oil and gas reserves have been estimated and independently verified with a higher degree of probability or smaller margin of error than resources, debt (reserve-based lending) can be raised to finance further development and production.

The successful completion of each exploration phase creates the opportunity for investors, depending on their investment strategy and risk appetite, to sell out their capital gains based on the increased value of the asset.

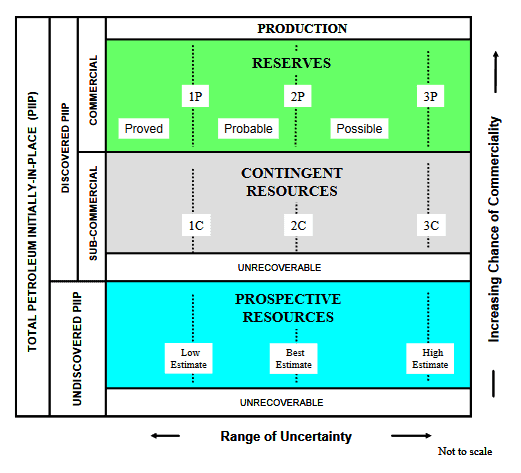

The below table sets out the oil and gas value chain which is used as the internationally recognised and accepted best practice.

Source: Guidelines for Application of the Petroleum Resources Management System

Example 1: In June 2023, based on their independent resources and reserves report, also called a competent persons report (CPR), done by Sproule (USA), Renergen Ltd, dual listed on the JSE and ASX, raised US$750 million (subject to conditions) for Phase 2 of their gas development project in South Africa. This is a significant milestone for the holders of South Africa’s first onshore gas production right.

Example 2: In June 2023, Kinetiko Energy Limited (ASX listed) announced, after conducting a significant exploration work program, that they will shortly be releasing their independent CPR. This report will set out Kinetiko’s gas reserves that would be capable of being produced and will form the basis of their onshore gas development and production work program and future capital raises which can now include debt finance (reserve-based lending). It is important to note that Kinetiko commenced exploration in South Africa with an AUS$10 million capital raise on the ASX for a 49% working interest and now has a market capitalisation of AUS$67 million.

2. Oil and gas exploration is high-risk, high-reward

The above statement is correct in general but need not be true specifically. Exploration in new or frontier areas, where companies have not previously explored and with little known geological data, fall within the high-risk, high-reward spectrum; whilst exploration risk in a specific country and/or area can be mitigated and reduced by a number of critical factors which increase the probability of success. These factors are as follows:

-

- Abundance of quality geological data;

- Proven geology demonstrating the presence of oil and/or gas;

- Positive exploration results by other companies within the same geological / geophysical complex; and

- Successful analogue companies.

Unfortunately, where all four of the above are present, usually in more developed exploration environments, the result is a significantly higher cost of entry, especially since governments often put higher value potential areas out for competitive bidding. It is also worth noting that advances in technology for exploration and development have been significant over the years; thereby increasing the probability of commercial success.

Example 3: Many past gas discoveries have been ignored where gas infrastructure was not present and a readily available gas market was not in close proximity to the discovery. Gas infrastructure and pipelines are long term investments requiring adequate throughput capacity or scale to be commercially viable. Advancements in technology, such as LNG (liquified natural gas) and small scale LNG, have made many previously unbankable projects bankable. The offshore gas discoveries in Mozambique only make commercial sense because of the scale and the exportability of that gas as LNG from floating LNG facilities. The domestic market in Mozambique does not have adequate scale or demand.

Example 4: The non-helium gas (CH4) produced by Renergen is currently being used for small scale LNG in South Africa; with Renergen delivering LNG from its facilities in Virginia, Free State to Consol Glass in Bellville, Western Cape over a distance of approximately 1300 kilometers.

3. Oil and gas exploration is too expensive

Unfortunately, this is true particularly for deep-water offshore exploration and, for this reason, only major and super major oil and gas companies can afford to engage in deep-water exploration. To mitigate deep-water exploration risk, exploration is usually done by joint venture partners who are able to spread the risk. As water depth increases, so does the cost of exploration.

Example 5: The Total E&P South Africa (“Total”) Brulpadda and Luiperd wells were drilled approximately 175 km offshore South Africa in water depths of 1.8 kilometers.

Commercial production is expected to commence in 2026; and peaking in 2037. The first well is recorded to have cost USD154 million. Total holds a 45% working interest in the discovery which has billion-barrel potential.

What this means is that the potential exploration target has to be sufficiently large in volume to justify the exploration cost and risk. It must also be noted, that even if deep-water discoveries are made, the development costs and getting the production to market can also represent significant cost and risk exposure. Not all successful oil and gas exploration companies have the scale and resources for offshore and/or deep-water exploration.

Many successful small cap companies focus on onshore or shallow waters where exploration and development costs are significantly lower. From a risk-reward perspective, exploration of smaller scale targets can be commercially viable, especially if a market is close. This holds true for onshore gas exploration, especially if a market already exist for the gas and new markets can be established. The costs for onshore exploration wells (core holes) for coal bed methane gas in South Africa range between R1.5 million to R2.5 million, depending on depth. The development and production costs for onshore gas is also significantly cheaper with growing gas demand for energy and power generation.

Example 6: Kinetiko Energy Limited, an ASX listed company, involved in onshore coal bed methane gas exploration reported prospective 2C gas resources of 4.9 TCF. 1.2 TCF of gas reserves is enough gas to power a 1000 MW power station for 20 years. As of today, Kinetiko’s market capitalisation is US$43 million which is less than one third of the cost of the Total first deepwater well offshore South Africa, and Total have drilled two.

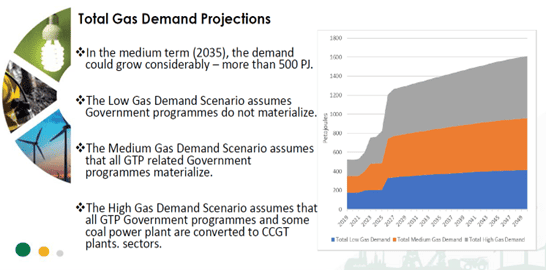

Example 7: Below is a table that sets out South Africa’s gas demand projections over the next 30 years as presented at the DMRE’s gas master plan industry stakeholder consultation workshop held in June 2023.

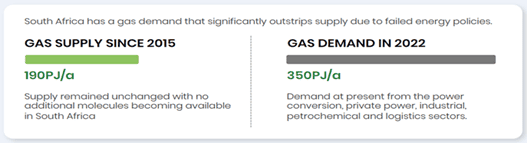

Example 8: The industrial gas users association-Southern Africa (“IGUA-SA”) stated concern in their 2022 annual report that gas demand in South Africa has outstripped supply. This concern is exacerbated due to the expected termination of the Sasol gas supply contract in 2026 based on the depletion of Sasol’s gas production from Mozambique and Sasol’s move to cleaner burning gas for their own facilities. See table below:

Example 9: In May 2023, the Petroleum Agency SA (“PASA”), South Africa’s oil and gas licensing agency advised that that shale gas moratorium that has been in place for more than 10 years will be lifted and that a shale gas bid round will be announced shortly. PASA estimates the Karoo Basin holds about 209 TCF of technically recoverable shale gas resources. Chief operating officer at PASA, Mr. Bongani Sayidini, stated that: “We are potentially looking at a minimum of about 10 shale gas blocks in the Karoo that will be released through competitive bidding.”

CONCLUSION

The aforementioned highlights only a few factors that must be considered when investing in the upstream oil and gas industry, specifically in South Africa. It also represents some of the potential opportunities that exist for investing in South Africa’s growing gas industry – both upstream and downstream provided financing institutions and venture capital institutions resource themselves with the necessary technical and commercial skillsets.

Example 10: It is not by coincidence that Standard Bank’s oil and gas division has played a significant role in financing oil and gas production projects in Africa, South Africa specifically. It is because they have invested in the necessary specialised skillsets and resourced them correctly. Below is an extract from their website:

Standard Bank is one of the largest oil and gas lenders in Sub-Saharan Africa given its on-the-ground presence in 20 countries across the continent. It’s Corporate and Investment Banking (CIB) division has a deep specialisation in Africa’s natural resources sector, where it has built up an enviable track record across the full spectrum of the mining, oil and gas value chain. These capabilities range from investment banking and advisory services to foreign exchange and commodities trading as well as the provision of working capital, cash management and forex solutions.

Some of the deals Standard Bank has been involved in during the last three years include the provision of US$ 225 million towards a US$ 2 billion facility for Petrobras O&G BV in Nigeria; US$ 175 million of a US$ 2.5 billion loan to Tullow Oil for Pan African expansion; provision of US$ 136 million of a US$ 1.5 billion facility for Kosmos Energy in Ghana, served as joint book – runner for the US$ 750 million Vivo IPO, US$75 million to Coral LNG in which Standard Bank was the only African Bank at financial close as well as supported in US$ 1.8 billion worth of trade flows relating to fuel / refined product imports into sub-Saharan Africa. Last year Standard Bank also provided US$ 80 million in reserve-based lending to Svenska Petroleum Exploration; US$ 136.5 million to Kosmos Energy Ghana, and US$ 40 million to Eland Oil & Gas in Nigeria.

“We have a wealth of knowledge across our team and have acted as mandated lead arranger, bookrunner, facility and security agent, and onshore bank for a number of international players in the industry,” says Mr. Kuti. “Our understanding of the continent is unrivalled, which coupled with our deep institutional knowledge base and industry expertise, means we are able to provide the necessary bespoke services required to successfully navigate the complexities of doing business in Africa’s frontier markets.”

Source: Africa to see continued oil & gas investment over next five years, says Standard Bank.

Part 7 of this opinion-editorial series will focus on other factors, such as fiscal terms and stability, political risk, gas market prices etc.

As Bastion continues to de-risk its onshore gas opportunities through intelligent exploration, we look forward to partnering with like-minded companies, development finance institutions and industry as joint venture partners, financiers, contractors and gas off-takers who like us consider this a worthwhile endeavor.

For more information please contact the undersigned at barrisford@bastionoil.com or info@bulwarkoil.co.za

Barrisford Petersen

Founder and Managing Director

Bastion Oil and Gas South Africa (Pty) Ltd

Bulwark Oil And Gas SA (Pty) Ltd

Rockit Energy (Pty) Ltd

LEGAL DISCLAIMER

DISTRIBUTION OF THIS DOCUMENT MAY BE RESTRICTED BY LAW. ACCORDINGLY, THIS DOCUMENT MAY NOT BE DISTRIBUTED IN ANY JURISDICTION EXCEPT IN ACCORDANCE WITH THE LEGAL REQUIREMENTS APPLICABLE TO SUCH JURISDICTION. IN PARTICULAR, YOU MAY NOT DISTRIBUTE, FORWARD, REPRODUCE, TRANSMIT OR OTHERWISE MAKE AVAILABLE THIS DOCUMENT OR DISCLOSE ANY INFORMATION CONTAINED IN IT OR CONVEYED DURING ANY ACCOMPANYING ORAL PRESENTATION (THE “INFORMATION”), IN WHOLE OR IN PART, DIRECTLY OR INDIRECTLY IN ANY JURISDICTION WHERE TO DO SO WOULD BE UNLAWFUL. FAILURE TO COMPLY WITH THESE RESTRICTIONS MAY CONSTITUTE A VIOLATION OF APPLICABLE SECURITIES LAWS. PERSONS INTO WHOSE POSSESSION THIS DOCUMENT COMES ARE REQUIRED BY THE COMPANY TO INFORM THEMSELVES ABOUT AND TO OBSERVE ANY SUCH RESTRICTIONS. NEITHER BASTION OIL AND GAS SOUTH AFRICA (PTY) LTD (INCLUDING ITS AFFILIATE BULWARK OIL AND GAS SA) (“COMPANY”) NOR ITS DIRECTORS, OFFICERS, EMPLOYEES, RESPECTIVE AFFILIATES, AGENTS OR ADVISERS ACCEPT ANY LIABILITY TO ANY PERSON IN RELATION TO THE DISTRIBUTION OR POSSESSION OF THIS DOCUMENT IN OR FROM ANY JURISDICTION.

The Document and the Information have been prepared by or on behalf of and is the sole property of the Company. The Information is being provided to you is not a complete record. The Information does not purport to be full or complete and does not constitute investment advice. No representation or warranty, express or implied, is given by or on behalf of the Company, its affiliates, agents or advisers or any other person as to, and no reliance may be placed for any purposes whatsoever on, the adequacy, accuracy, completeness, fairness or reasonableness of the Information. None of the information has been independently verified by the Company, its affiliates, agents or advisers or any other person, and no liability or responsibility whatsoever is accepted by any of them for any loss howsoever arising, directly or indirectly, from any use of the Information or otherwise arising in connection therewith. The Company, its affiliates, agents and advisers do not undertake and are not under any duty to update this Document or to correct any inaccuracies in the Information which may become apparent or to provide you with any additional information.

The sole purpose of this Document is to provide background information to assist you in obtaining a general understanding of the business of the Company. This Document does not constitute an offer to sell, or a solicitation of an offer to buy or subscribe for, securities of the Company in any jurisdiction. It is not intended to provide the basis of any investment decision, financing or any other evaluation and is not to be considered as a recommendation by the Company, its affiliates, agents or advisers that any recipient of this Document purchase or subscribe for any securities in the Company. Each recipient of this Document contemplating any investment in the Company is required to make and will be deemed to have made its own independent investigation and appraisal of the business, results of operations, financial condition, liquidity, performance and prospects of the Company and the merits and risks of an investment in the securities of the Company. The delivery of this Document at any time does not imply that the information in it is correct as of any time after its date, or that there has been no change in the business, results of operations, financial condition, liquidity, performance and prospects of the Company since that date and no obligations is accepted to update any such information after the date of the Document. No person affiliated with the Company, their directors, officers, employees, respective affiliates, agents or advisers has been authorised to give any information or to make any representation not contained in this Document and, if given or made, such information or representation must not be relied upon. This Document may contain forward-looking statements, including, but not limited to, statements as to the Company’s business, results of operations, financial condition, liquidity, performance and prospects and trends and developments in the markets in which the Company operates. Forward-looking statements include all statements other than statements of historical fact and in some cases may be identified by terms such as “targets”, “believes”, “expects”, “anticipates”, “estimates”, “aims”, “intends”, “will”, “may”, “would”, “could” or, in each case, their negative or comparable terms. By their nature, forward-looking statements involve risk and uncertainty because they relate to future events and circumstances that may or may not occur. Several factors, which may be beyond the control of the Company, its affiliates, agents and advisers, could cause actual results and developments to differ materially from those expressed or implied by the forward-looking statements. Forward-looking statements in this Document reflect the Company’s view with respect to future events as at the date hereof and are subject to known and unknown risks, uncertainties and assumptions relating to the Company’s operations, results of operations, financial condition, growth, strategy, liquidity and the markets in which the Company operates. No assurances can be given that the forward-looking statements in this Document will be realised. Forward-looking statements are not guarantees of future performance. The Company, its affiliates, agents and advisers undertake no obligation and do not intend to update any forward-looking statements in this Document to reflect events or circumstances after the date of this Document.

Recent Comments